1.0 Introduction

“Non-financial reporting (NFR)” plays an important role in disclosing information related to companies' like BDO LLP’s financial performance, ESG factors, and its impact on responsible practices and sustainability practices. There are unprecedented demands for the “environmental, social, and governance (ESG) performance”, but so many business fail at managing data integrity. That is why, the measurement and reporting of “non-financial information” must be precise, complete and not misleading to avoid negative consequences for the company resulting from low-quality information (Fiandrino et al. 2022). Therefore, the following section identifies the difficulties that are connected with quality and reliability of data in “non-financial reporting” of “BDO LLP” with its benefits and drawbacks. This report also examines some academic literature in real-world situations to identify the effectiveness of the challenges of reliability and data quality that are faced in preparing “non-financial reporting”.

2.0 Discussion Analysis

Impacts of “non-financial reporting”

“Non-finial reporting” is a form of reporting that is important more on the extra-financial performance of a company and its “environmental, social, and governance” related information rather than financial performance. Such reports may contain information on “carbon footprint”, labor relations, social impact, diversity and communication of the company’s governance structures. Over the years, different groups such as the investors, customers and regulators have placed high value on “non-financial reporting” (Lakshan et al. 2022). However, “non-financial data” has its complexities that make it difficult to have a reliability and quality of data. In contrast to financial data, “non-financial data” is not normalized and, in most instances, the data is gathered by questionnaires from respondents of companies (Sierra García et al. 2022). Thus the knowledge of the issues related to increasing the reliability of such data as accurate, consistent and complete is considered to be vital for developing the concept of the “sustainability accounting”.

2.1 Critical evaluation of the Chosen Issue of reliability and quality of data in non-financial reporting

The need for credibility and quality of “non-financial information” is consequently a major determinant of the reliability and accuracy of sustainable information. In recent days, the necessity of the “non-financial reporting” increased significantly. In recent days, it also found that “the United Nations Sustainable Development Goals (2015)” includes the universal framework that maintains CSR activities and sustainable objectives. In this way, the companies can maintain the data reliability and the quality (Lakshan et al. 2022). It becomes the problem to investors, regulators and consumers because it affects the flow of right information with regard to sustainable practices by a given firm like BDO LLP. In this section, the issues related to the reliability and quality of data for “non-financial reporting” are identified for discussion of the challenges that are faced in producing “non-financial reporting”.

Challenges from the Quality and Reliability Data

Standardization problem

“Non-financial information” poses a major problem to its quality since there are no universal set of rules on how the information should be reported. Currently, there are diverse frameworks that economic entities may use when reporting about the ESG activities, including GRI, SASB, and TCFD, which results in diversified approaches to presenting data (Dimes & Molinari, 2024). The absence of standardization hampers the ability of players in the chain to compare data with other organizations, industries, or regions.

Advantages

Suitability: Employers can select regulations that may be suitable for their ability and objectives.

Positive aspect: The broad dissemination of reporting requirements offer the opportunity to various corporations to introduce creative practices in to demonstrate their sustainability initiatives.

Disadvantages

Absence of standardization: Though “non-financial information” can be diverse, there is no consistent reporting format for the information thus making it difficult for the shareholders to believe in the information being provided.

Standard evolution: It may be challenging for an organization to coordinate the compliance of reporting on various framework, thus provoking ambiguity and challenges.

1. Subjectivity challenges

The organization has quite a lot of discretion in both what to report and how to quantify the sustainability management impact (Omran et al. 2021). This can make the information quite relative based on the desire that a company has to share more information about the sustainability practices.

Advantages

Developing: Companies ensuring the promotion of ESG issues as relevant to the company’s operations as possible.

Specificity: Companies can provide relevant data on aspects of ESG performance that are most important to it.

Disadvantages

Selective reporting: Only positive information may be revealed since negative information may harm the company constituting manipulation.

Misinformation: Due to the lack of clear rules for managing such information, a company may come up with distorted information to improve its image.

2. Problems from availability of accurate data

It proves difficult to acquire accurate “non-financial data” mainly because most organizations extract the information from internal employees or contractors (Turzo et al. 2022). Unfortunately, this and all other types of enormous information, in advent or manipulated, compromise the credibility of a firm’s sustainability report.

Advantages

ESG Reporting: Organizations like BDO LLP have had established detailed systems in the gathering of data for the preparation of their ESG reports.

Improved Decision making: The best quality and timely data leads to better sustainability decisions in different business organizations.

Disadvantages

Inaccuracy: Since not all the devices are standard, the data collected may be inconsistent or even incorrect.

Resource Intensive: Most of the data requires validation in terms of time and resources used before coming up with an accurate result.

3. Regulatory problems

The other task failing current financial reporting is usually driven by the regulators to presenting transparent and accountable information which is non-financial information. However, there are differences in these regulations by country thus making the compliance issues complicated particularly for the international firm.

Advantages

Regulatory reasons help to enhance accountability: The set requirements affect the collection and reporting of data.

Legal Frameworks: Regulations improve the image of various bodies by increasing the level of transparency.

2.2 Literature review

According to Turzo et al. (2022) did the research on several challenges faced during “non-financial reporting”. This research investigates the development of “non-financial reporting policies” or NFR for short, to consider some standards including “CSR, GRI, and IR” (Turzo et al. 2022). It emphasizes on the problem attributed by the lack of standard, which creates disparity in terms of NFR implementation throughout the world. In the study, bibliometric analysis is employed to ascertain that major themes of NFR research have been addressed; firm-level variables, “corporate governance”, and environmental reporting.

Similarly, Mysak et al. (2021) discusses the increasing need for ecological data in business due to a change in the business environment, particularly due to climatic changes and natural disasters. It suggests enhancing the qualities of ecological management reporting relative to information presentation and accuracy of the non-financial information (Mysak et al. 2021). In the study, the focus is on “GRI Standards”, and to improve the quality of the report and support “decision-making”, it is suggested to disclose more data on the consumption of resources and energy, preservation of the environment, releases, and waste management.

According to Schröder, (2022) study shows that the quality of implemented NFRs is average; however, it has improved after three years. The present study’s findings are “NFRQ determinants”; the experience architectures, format pick-hand option and the framework (Schröder, 2022). These indicated relatively promising knowledge are highly beneficial towards adopting a better approach to “NFR practices”, as well as updating knowledge for further EU NFR policy & regulation improvements.

2.3 Reflection

Gibb’s reflective model helps me to understand the reflections on learning understanding on sustainability approaches in “Accounting to Plannet”.

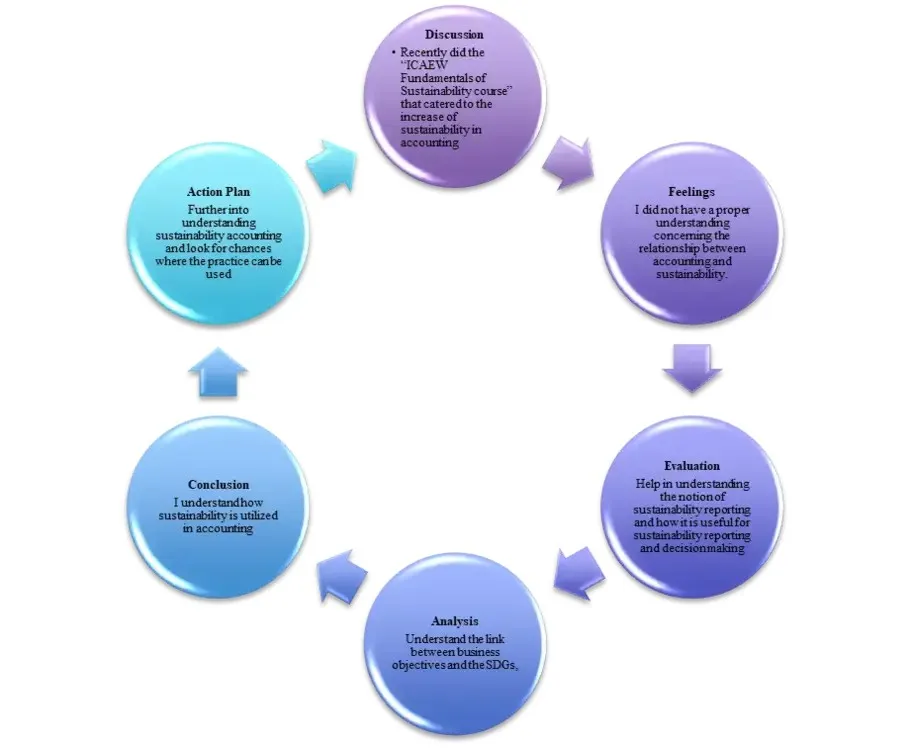

Figure 1: Gibb’s reflective model

(Source: Self-created in MS Word)

Discussion

I recently did the “ICAEW Fundamentals of Sustainability course” that catered to the increase of sustainability in accounting. Some of the areas covered included the “United Nations Sustainable Development Goal (SDGs)” and Sustainability reporting, Information on how accountants are advancing towards the achievement of sustainability goals was also availed.

Feelings

In the beginning, I did not have a proper understanding concerning the relationship between accounting and sustainability. Yet, the changing motivation occurred as the course evolved and I saw that accountants have the potential to engage in the effective decision-making on business sustainability. I would describe that I have sensed the great potential of the topic and at the same time experienced the concerns regarding the potential lack of preparedness for such reporting.

Evaluation

In the third “evaluation stage” I evaluate the challenges that are faced from the reliability and data quality. The course also help in understanding the notion of sustainability reporting and how it is useful for sustainability reporting and decision making. At the same time, with focus on the SDG and their applicability to businesses, I use learned the difficulties of a high quality and consistent sustainability data.

Analysis

There is no doubt that the building was a necessity and that accountants can contribute significantly towards ensuring that the sustainability reports are accurate. The course also helped the students understand the link between business objectives and the SDGs, which has become more relevant for securing investment and gaining legitimacy.

Conclusion

As a result of my experience, I understand how sustainability is utilized in accounting and would like to advance my understanding of sustainability indicators and reporting framework.

Action Plan

I will also progress further into understanding sustainability accounting and look for chances where the practice can be used.

3.0 Conclusion

Despite the increasing pressure from stakeholders on reporting organizations to provide information that they require, the accuracy and credibility of information disclosed in “non-financial reports” is one of the headaches of reporting organizations like BDO LLP. Main challenges are lack of standardization, subjectivity of the results, and significant data accuracy concerns, but these can be addressed by increasing the measure’s standardization, third-party verification, or clearer rules. As a part of it, it is crucial to achieve assurance over high-quality non-financial data for creating trust and enhancing decision-making for the advancement of corporate sustainability.

Struggling with your Accounting Planet Non-Financial Reporting Assignment? Get expert guidance from our professional online assignment help and achieve top grades with ease. Our specialists ensure high-quality, well-researched solutions that save your time and boost your confidence. Don’t let complex topics hold you back let us help you succeed today!

Reference List

Journals

- Dimes, R., & Molinari, M. (2024). Non-financial reporting and corporate governance: a conceptual framework. Sustainability Accounting, Management and Policy Journal, 15(5), 1067-1093. [Retrieve from: https://www.emerald.com/insight/content/doi/10.1108/sampj-04-2022-0212/full/html][Retrieve on: 12.03.2025]

- Fiandrino, S., Gromis di Trana, M., Tonelli, A., & Lucchese, A. (2022). The multi-faceted dimensions for the disclosure quality of non-financial information in revising directive 2014/95/EU. Journal of Applied Accounting Research, 23(1), 274-300. [Retrieve from: https://www.emerald.com/insight/content/doi/10.1108/JAAR-04-2021-0118/full/html][Retrieve on: 12.03.2025]

- Lakshan, A. M. I., Low, M., & de Villiers, C. (2022). Challenges of, and techniques for, materiality determination of non-financial information used by integrated report preparers. Meditari Accountancy Research, 30(3), 626-660. [Retrieve from: https://www.emerald.com/insight/content/doi/10.1108/MEDAR-11-2020-1107/full/html][Retrieve on: 12.03.2025]

- Lakshan, A. M. I., Low, M., & de Villiers, C. (2022). Challenges of, and techniques for, materiality determination of non-financial information used by integrated report preparers. Meditari Accountancy Research, 30(3), 626-660. [Retrieve from: https://www.emerald.com/insight/content/doi/10.1108/MEDAR-11-2020-1107/full/html][Retrieve on: 12.03.2025]

- Mysaka, H., Derun, I., & Skliaruk, I. (2021). The role of non-financial reporting in modern ecological problems updating and solving. Journal of Environmental Management & Tourism, 12(1), 18-29. [Retrieve from: https://www.academia.edu/download/87635951/2_HannaMYSAKA_18_29_JEMT_Issue149Spring20212.pdf][Retrieve on: 12.03.2025]

- Omran, M., Khallaf, A., Gleason, K., & Tahat, Y. (2021). Non-financial performance measures disclosure, quality strategy, and organizational financial performance: a mediating model. Total Quality Management & Business Excellence, 32(5-6), 652-675. [Retrieve from: https://www.tandfonline.com/doi/abs/10.1080/14783363.2019.1625708][Retrieve on: 12.03.2025]

- Schröder, P. (2022). Mandatory non-financial reporting in the banking industry: assessing reporting quality and determinants. Cogent Business & Management, 9(1), 2073628. [Retrieve from: https://www.tandfonline.com/doi/abs/10.1080/23311975.2022.2073628][Retrieve on: 12.03.2025]

- Sierra García, L., Bollas-Araya, H. M., & García Benau, M. A. (2022). Sustainable development goals and assurance of non-financial information reporting in Spain. Sustainability Accounting, Management and Policy Journal, 13(4), 878-898. [Retrieve from: https://www.emerald.com/insight/content/doi/10.1108/sampj-04-2021-0131/full/html][Retrieve on: 12.03.2025]

- Turzo, T., Marzi, G., Favino, C., & Terzani, S. (2022). Non-financial reporting research and practice: Lessons from the last decade. Journal of Cleaner Production, 345, 131154. [Retrieve from: https://www.sciencedirect.com/science/article/pii/S0959652622007867][Retrieve on: 12.03.2025]

Go Through the Best and FREE Samples Written by Our Academic Experts!

Native Assignment Help. (2026). Retrieved from:

https://www.nativeassignmenthelp.co.uk/accounting-planet-non-financial-reporting-assignment-46962

Native Assignment Help, (2026),

https://www.nativeassignmenthelp.co.uk/accounting-planet-non-financial-reporting-assignment-46962

Native Assignment Help (2026) [Online]. Retrieved from:

https://www.nativeassignmenthelp.co.uk/accounting-planet-non-financial-reporting-assignment-46962

Native Assignment Help. (Native Assignment Help, 2026)

https://www.nativeassignmenthelp.co.uk/accounting-planet-non-financial-reporting-assignment-46962

- FreeDownload - 41 TimesMarketing Plan At Tesco PLC Case Study

Introduction to Tesco's Marketing Plan Background Marketing is a...View or download

- FreeDownload - 40 TimesLCBB5003 Management Economics Assignment Example

LCBB5003 Management Economics Introduction-LCBB5003 Management Economics Fast...View or download

- FreeDownload - 40 TimesCBU610 Business Strategy and Sustainability Assignment

Assessment 1 Introduction This report aims to evaluate the strategic position...View or download

- FreeDownload - 40 TimesL7 BA70012E Project Management Assignment sample

Project Management: L7 BA70012E The UK’s top-notch assignment writing...View or download

- FreeDownload - 40 TimesFinancial Statement Assignment Sample

Financial Statement Assignment Introduction: Financial Statement Financial...View or download

- FreeDownload - 43 TimesPlagiarism in Academia and Business: Challenges and Best Practices

Introduction Plagiarism is representation of another person’s thoughts,...View or download

-

100% Confidential

Your personal details and order information are kept completely private with our strict confidentiality policy.

-

On-Time Delivery

Receive your assignment exactly within the promised deadline—no delays, ever.

-

Native British Writers

Get your work crafted by highly-skilled native UK writers with strong academic expertise.

-

A+ Quality Assignments

We deliver top-notch, well-researched, and perfectly structured assignments to help you secure the highest grades.