Report Summarising Group Strategy for Dealing with Project Particulars and Errors in the Bill of Quantities (BoQ)

Introduction

The following is the strategy the group utilised in order to deal with the project particulars and the mistakes in the BoQ of Construction of Access Road for Residential Development. This is more concentrated in the quest to correct the tenders calculations, the mistakes and the work to be done within the project lifespan.

1. Project Particulars Strategy

The key project particulars are:

- Form of Contract: NEC4 Option B.

- Contract Duration: 40 weeks.

- Retention: 5% of contract sum.

- Delay Damages: £3,000 per week.

Students seeking Assignment Help can master construction costing, project particulars, and Bill of Quantities (BoQ) error resolution. Our expert insights assist in crafting detailed project plans, managing tenders effectively, and controlling costs, ensuring academic excellence and practical knowledge for construction management courses

To effectively handle these project particulars, the group has formulated the following strategy:

A. Contract and Duration

- The time period taken to complete the work order has been estimated with respect to the usual onsite activities like site mobilisation, excavation work, installing drainages, road construction and demobilisation. EACH phase is divided into reasonable tasks and reasonable resources are assigned to them to meet the balanced workload at each phase of the project (Pan & Zhang, 2021).

- Microsoft Project for project management has been adopted to develop the Gantt chart for tasking; this completes all the milestones within the time line projected.

B. Cost Control and Monitoring

- To ensure practicality is accorded to the project budget, cash flow forecasts have been established for every day of the project period. Budgeting allows the control of expenses and guarantees that any amount is expected or required during the project implementation.

- Estimates of preliminaries and overheads are made accurately, while alternatives of indirect expenses, including insurance, mobilisation, or demobilisation, are included into the tender sum to prevent differences.

C. Risk Management

- Delay Damages: The group has ensured that risk barriers have been integrated with some critical phases of the project like the installation of drainage Age and asphalt paving which are known to be probably delayed most of the time. A few examples where costs have been incorporated into the cash flow forecast are £3,000 per week of delay damages.

- Mitigating Potential Errors: Problems that may have been observed in the BoQ include inadequate descriptions or omitted quantities have been confirmed with the project manager and the client when preparing the tender documents (Holm & Schaufelberger, 2021).

2. Errors in the Bill of Quantities (BoQ)

The group has identified several potential errors and assumptions in the BoQ and devised strategies to address them:

A. Ambiguities in Quantity Measurements

Uncertainty is also present for some of the measured quantities in the BoQ such as trench dimensions (depth and width), quantity of fill material(s).

- Strategy: To power its models, the group has made reasonable postulates to complete these gaps.Having looked at the qualifications made when estimating the KL model, the features that complete the gaps thought to be distinctive of the AS model are given below (Elmousalami, 2020). For instance, it has been assumed that trench depth on drain runs will be between 1500mm up to 2000mm for the first part and 2000mm up to 2500mm for the next part. Such assumptions are formulated with reference to common practise in the sector and the conditions existing at the project site (Deng et al., 2021).

B. Missing Items in the BoQ

- The BoQ was silent on the testing and commissioning of specific drainage systems that are important in quality deliveries.

- Strategy: The group assumed that an item cost for pressure testing to BS 8005 and EN1610 for drainage testing based on industry practises.

C. Inconsistent Material Costs

- Some of the material types in the BoQ have high cost variations that cannot be justified. For example, uPVC pipes and precast concrete kerbs have price differences per unit, and it is not clear as to what the units refer to.

- Strategy: The group then employed the average material cost rates and compared them to the benchmark prices for comparable constructions. The actual rates applied used included £4.75/m for uPVC 100mm diameter pipe and £52.35/m³ for precast concrete kerbs.

D. Overestimated Resource Requirements

- Quantities for some of the labour and plant resource consisted on some lists without explanation of quantities. For instance, the number of labourers to perform several phases, including the installation of drainage, was not consistent with the standard productivity per equipment (Chakraborty et al., 2020).

- Strategy: The group engaged in a resource smoothing using the available information by focusing the number of workers and machine hours which was expected to deliver the planned output for example of the excavator per hour, labour hours per task.

3. Assumptions and Adjustments

Given the complexity of the BoQ, certain assumptions were necessary to complete the tender:

- Waste and Compaction: They assumed 5% wastage for all items such as crushed rock and hardcore. Further, a compaction factor of 15% for granular materials was incorporated in the computation, as observed in constructions (Allouzi et al., 2020).

- Plant and Equipment Usage: The group estimated 80hs for the 20-tonne excavator and 60hs for the 10-tonne roller depending on the presumed time to complete tasks of excavation and compaction.

4. Strategy for Addressing Project Changes

- Thus, the group has come up with a means of dealing with any alterations in the concerned project scope, as may be witnessed in the executing phase. These are to keep a contingency fund and to also have the necessary communication with the client to address any controversy arising in the BoQ or alteration in the project specifications instantly.

- Reallocation of resources during the course of work becomes easy through the use of project management software (Microsoft Project).

Conclusion

The group has adopted an holistic strategy to manage the project specifics and any mistakes in the Bill of Quantities. Thus, the group believes that with reasonable assumptions, the propriety of tested resource demands, and the subsequent agreement with the client, the project shall be achieved on time and within budget. The project is further kept on track for detailed forecasting and planning tools that are used to identify likely risks or uncertainty that may arise during the processes.

Tender Form

Project: Construction of Access Road for Residential Development

Contract Type: NEC4 Option B

Duration: 40 weeks

Retention: 5%

Delay Damages: £3,000 per week

Tender Summary

|

Category |

Cost (£) |

|

Supervision & Staff |

£139,200 |

|

Accommodation & Services |

£5,000 |

|

Site Mobilisation & Demobilisation |

£5,000 |

|

Small Tools and Traffic Management |

£84,800 |

|

Insurances |

£2,500 |

|

Head Office Overheads |

£43,750 |

|

Profit |

£50,000 |

|

Excavating and Filling |

£3,768 |

|

Drainage Runs |

£924 (165m) |

|

Drainage Runs (deep trenches) |

£266 (56m) |

|

Manholes |

£1,316 (10 nr) |

|

Connections to live sewer |

£9.50 (2 items) |

|

Testing and Commissioning |

£477.40 |

|

Kerbs (including joints and haunching) |

£2,083.53 |

|

Other Works |

£660,648 |

|

Total Tender Amount |

£960,243.93 |

|

Final Tender Offer (Rounded) |

£1,000,000 |

Proposed Timeline

|

Activity |

Duration (Weeks) |

|

Site Mobilisation |

2 |

|

Site Demobilisation |

2 |

|

Small Tools and Traffic Management |

2 |

|

Excavation and Site Preparation |

3 |

|

Drainage Installation |

4 |

|

Manholes |

2 |

|

Connections to live sewer |

1 |

|

Testing and Commissioning |

2 |

|

Kerb Installation |

4 |

|

Road Construction and Asphalt Surfacing |

8 |

|

Concrete Footways and Finishing Works |

10 |

Total Project Duration: 40 Weeks

Timeframe

Contract Duration: 40 weeks

The project will be delivered on schedule with a completion date calculated as:

Signing date + 40weeks = contractual completion date.

Terms and Conditions

- >

- All elements of the tender sum involve costs of labour, plant, materials, and overheads.

- As much as is reasonably practicable, given a prescribed schedule, work will be delivered at the timeframe suggested.

- Some of the things that have to be decided before signing the contract.

- The conditions of scope or any circumstance that is not foreseen will be handled by a legal change order.

Analytical bill of quantity

Assume a standard working week of 5 days (Monday to Friday).

Contract duration: 40 weeks.

Roles, Rates, and Total Hours for Supervision & Staff:

|

Role |

Utilisation |

Rate (£/day) |

Total days at work |

Total Cost (£) |

|

Project Manager |

100% Utilisation |

330 |

40×5 = 200 |

66000 |

|

Site Engineer |

100% Utilisation |

240 |

40×5 = 200 |

48000 |

|

Quantity Surveyor |

20% Utilisation |

330 |

8×5 = 40 |

13200 |

|

Health and Safety Manager |

20% Utilisation |

300 |

8×5 = 40 |

12000 |

Total Supervision & Staff Hours:

- Total Hours: 200+200+40+40 = 480 hours

- Total Staff Costs: 66,000+48,000+13,200+12,000=£139,200

|

Category |

Details |

Rate (£) |

Duration/Quantity |

Total Cost (£) |

|

Accommodation & Services |

Weekly cost of site accommodation |

£125/week |

40 weeks |

125×40=5,000 |

|

Site Mobilisation |

Assumed lump sum cost for setting up site |

£3,000 (assumed) |

1 (one-time cost) |

3,000 |

|

Site Demobilisation |

Assumed lump sum cost for clearing site |

£2,000 (assumed) |

1 (one-time cost) |

2,000 |

|

Small Tools & Equipment |

Daily cost for tools and traffic management equipment |

£299/day |

5days/week × 40weeks = 200 days |

59,800 |

|

Traffic Management Services |

Additional traffic control and signage requirements |

£125/day |

5days/week × 40weeks = 200 days |

25000 |

Preliminaries

Preliminaries include initial setup, project accommodation, insurance, and other indirect costs.

|

Item |

Quantity |

Rate (£) |

Total (£) |

|

Accommodation (weekly) |

40 weeks |

£125/week |

£5,000 |

|

Site Mobilisation |

Lump sum |

£3,000 |

£3,000 |

|

Site Demobilisation |

Lump sum |

£2,000 |

£2,000 |

|

Insurance |

Contract value |

0.50% |

£2,500 |

|

Total Preliminaries |

£12,500 |

Direct Costs

These include the resources required to execute the works as per the specifications.

Labour Costs

|

Role |

Total Hours |

Hourly Rate (£) |

Total (£) |

|

Project Manager |

1,600 |

£41.25 |

£66,000 |

|

Site Engineer |

1,600 |

£30.00 |

£48,000 |

|

Quantity Surveyor |

320 |

£41.25 |

£13,200 |

|

Health & Safety Manager |

320 |

£37.50 |

£12,000 |

|

Skilled Operatives |

1,200 |

£24.70 |

£29,640 |

|

Total Labor Costs |

£168,840 |

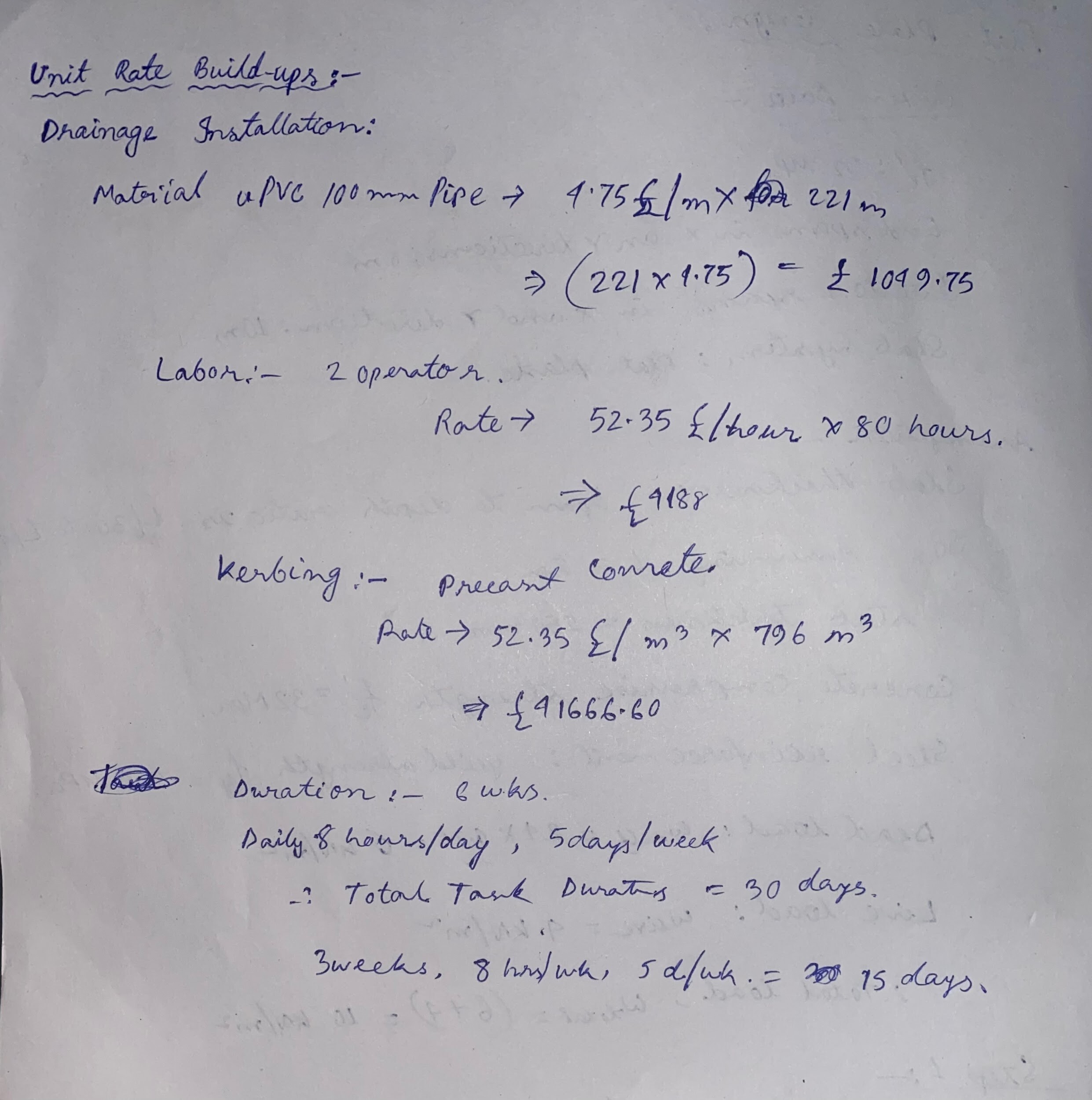

Material Costs

|

Material |

Quantity |

Rate (£) |

Total (£) |

|

uPVC 100mm Pipe |

221m |

£4.75/m |

£1,049.75 |

|

Precast Concrete Kerbs |

796m3 |

£52.35/m3 |

£41,666.60 |

|

Crusher Run Stone |

200 tonnes |

£14.20/tonne |

£2,840.00 |

|

Imported Hardcore |

300 tonnes |

£14.95/tonne |

£4,485.00 |

|

Concrete for Kerb Haunching |

100m3 |

£86.70/m3 |

£8,670.00 |

|

Total Material Costs |

£58,711.35 |

Plant and Equipment Costs

|

Equipment |

Usage Hours |

Rate (£) |

Total (£) |

|

20-Tonne Excavator |

80 |

£52.35/hour |

£4,188 |

|

10-Tonne Roller |

60 |

£33.65/hour |

£2,019 |

|

Asphalt Spreader |

20 |

£89.70/hour |

£1,794 |

|

Traffic Management Tools |

200 days |

£299/day |

£59,800 |

|

Total Plant Costs |

£67,801 |

Overheads and Profit

|

Category |

Rate |

Total (£) |

|

Head Office Overheads |

8.75% of cost |

£43,750 |

|

Profit |

10% of cost |

£50,000 |

Summary of Resource Budgets

|

Category |

Total (£) |

|

Preliminaries |

£12,500 |

|

Labor |

£168,840 |

|

Materials |

£58,711.35 |

|

Plant and Equipment |

£67,801 |

|

Overheads and Profit |

£93,750 |

|

Grand Total |

£401,602.35 |

Overheads Contribution

Indirects also help the contractor to keep their business running and at the same time executing the project with ease. These include expenses which is incurred in running the business and other ancillary support to the project. The overheads are apportioned for this project in relation to the company’s total turnover and the amount of the resources have been allocated to the tender.

- >

- Calculation Basis

- Annual overheads are £7,000,000, turnover is £80,000,000.

- Overhead percentage: 7,000,000/80,000,000=8.75%

- For this project, based on the tender value of £1,000,000, overheads are calculated as:

- 1,000,000×0.0875=£43,750

- >

- Components of Overheads

- Administrative Costs: Costs for administrative support workers, including clerical and secretarial personnel, and other employees in the accounting, legal and administrative departments.

- Corporate Expenses: Expenses related to insurance, licences and regulation, compliance etc.

- Infrastructure Maintenance: Hire of premises, light,Heat, power and Computer ‘plug and play’ needs to run the office efficiently.

- Business Development: Marketing, tendering expense, and management of the relationship growers share with their clients.

- >

- Justification

The percentage is in compliance with overhead contribution standards so that the contractor can sustain profitability in the provision of the indirect costs. This allocation is strategic to try to ensure continuity of support of the project.

Preliminaries (On-Costs): Calculations & Justification

On-costs or preliminaries are project related costs for the actualization of the works but which does not relate to the works. These costs are calculated and justified as follows:

- >

- Site Accommodation

- Weekly rate: £125/week.

- Contract duration: 40 weeks.

- Total Cost: £125 × 40 = £5,000.

- Justification: This is because site accommodation is required to house the site manager’s offices, meeting facilities and file storage space for documentations.

- Mobilisation and Demobilisation

- Mobilisation: £3,000 (assumed).

- Demobilisation: £2,000 (assumed).

- Total Cost: £3,000 + £2,000 = £5,000.

- Justification: These large, up-front costs include the transportation of equipment, the installation of facilities and the removal of debris at the end of a project.

- Small Tools and Traffic Management

- Daily rate for tools and traffic management: £299/day.

- Working days: Five days a week x forty weeks = Two hundred days.

- Total Cost: £299 × 200 = £59,800.

- Justification: Such costs include the machines and structures needed for site safety and traffic control, as well as for meeting relevant laws.

- Insurances

- Rate: 0.It stated that its supply contracts required suppliers to provide rebates of 50% of the contract value up to a limit of £1,000,000.

- Total Cost: £1,000,000 × 0.005 = £2,500.

- Justification: It is an indemnifying agreement against probable mishaps in construction work by absorbing the costs such as liabilities, damages and risks.

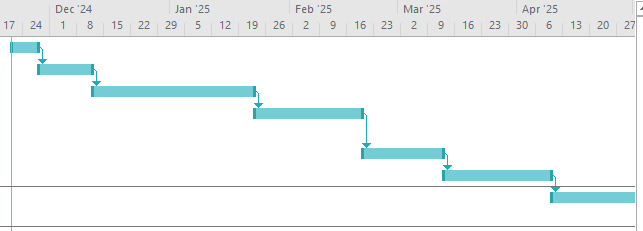

Gantt Chart

|

Task Name |

Start |

Duration |

Finish |

Baseline Cost (£) |

Cost (£) |

|

Project Mobilisation |

Week 1 |

1 week |

Week 1 |

£3,000 |

£3,000 |

|

Site Preparation |

Week 2 |

2 weeks |

Week 3 |

£5,000 |

£5,000 |

|

Drainage Installation |

Week 4 |

6 weeks |

Week 9 |

£65,000 |

£68,000 |

|

Sub-Base Preparation |

Week 10 |

4 weeks |

Week 13 |

£30,000 |

£32,000 |

|

Kerbing and Edging |

Week 14 |

3 weeks |

Week 16 |

£15,000 |

£16,500 |

|

Asphalt Paving |

Week 17 |

4 weeks |

Week 20 |

£80,000 |

£85,000 |

|

Landscaping and Final Works |

Week 21 |

5 weeks |

Week 25 |

£25,000 |

£27,000 |

|

Testing and Commissioning |

Week 26 |

2 weeks |

Week 27 |

£10,000 |

£10,500 |

|

Site Demobilisation |

Week 28 |

1 week |

Week 28 |

£2,000 |

£2,000 |

(Source: MS Project)

Cashflow Forecast

|

Week |

Activity |

Cost (£) |

Cumulative Cost (£) |

|

1 |

Project Mobilisation |

3,000 |

3,000 |

|

2-3 |

Site Preparation |

5,000 |

8,000 |

|

4-9 |

Drainage Installation |

68,000 |

76,000 |

|

10-13 |

Sub-Base Preparation |

32,000 |

108,000 |

|

14-16 |

Kerbing and Edging |

16,500 |

124,500 |

|

17-20 |

Asphalt Paving |

85,000 |

209,500 |

|

21-25 |

Landscaping and Final Works |

27,000 |

236,500 |

|

26-27 |

Testing and Commissioning |

10,500 |

247,000 |

|

28 |

Site Demobilisation |

2,000 |

249,000 |

Monthly Cashflow

Assuming work progresses consistently within each month:

|

Month |

Cost (£) |

Cumulative Cost (£) |

|

Month 1 |

8,000 |

8,000 |

|

Month 2 |

38,000 |

46,000 |

|

Month 3 |

32,000 |

78,000 |

|

Month 4 |

51,500 |

129,500 |

|

Month 5 |

85,000 |

214,500 |

|

Month 6 |

27,000 |

241,500 |

|

Month 7 |

7,500 |

249,000 |

Cash Flow Insights

- >

- Peak Expenditure: Asphalt paving and drainage installation account for the highest costs (Weeks 4–20).

- Cash Reserves: Ensure availability of £85,000 during the asphalt paving phase (Month 5).

- Cumulative Total: Total cash requirement is £249,000 (aligned with cost breakdown)

Individual Build-ups Summary

This section outlines the contributions of each group member to the project. It provides details on their individual unit rate build-ups, task durations, and the assumptions they made in terms of waste, laps, bulking, compaction, and other factors.

Conclusion

Each group member has contributed to specific aspects of the project, ensuring that unit rates are calculated based on industry standards, assumptions are made where necessary, and task durations are realistic and achievable. These individual contributions, along with the collective effort to manage waste, compaction, and other project variables, ensure the accuracy and feasibility of the final tender offer.

Reference List

Journals

Allouzi, R., Al-Azhari, W. and Allouzi, R., 2020. Conventional construction and 3D printing: A comparison study on material cost in Jordan. Journal of Engineering, 2020(1), p.1424682.

Chakraborty, D., Elhegazy, H., Elzarka, H. and Gutierrez, L., 2020. A novel construction cost prediction model using hybrid natural and light gradient boosting. Advanced Engineering Informatics, 46, p.101201.

Deng, M., Menassa, C.C. and Kamat, V.R., 2021. From BIM to digital twins: A systematic review of the evolution of intelligent building representations in the AEC-FM industry. Journal of Information Technology in Construction, 26.

Elmousalami, H.H., 2020. Artificial intelligence and parametric construction cost estimate modeling: State-of-the-art review. Journal of Construction Engineering and Management, 146(1), p.03119008.

Holm, L. and Schaufelberger, J.E., 2021. Construction cost estimating. Routledge.

Pan, Y. and Zhang, L., 2021. Roles of artificial intelligence in construction engineering and management: A critical review and future trends. Automation in Construction, 122, p.103517.

Go Through the Best and FREE Samples Written by Our Academic Experts!

Native Assignment Help. (2026). Retrieved from:

https://www.nativeassignmenthelp.co.uk/construction-costing-boq-error-management-sample-42897

Native Assignment Help, (2026),

https://www.nativeassignmenthelp.co.uk/construction-costing-boq-error-management-sample-42897

Native Assignment Help (2026) [Online]. Retrieved from:

https://www.nativeassignmenthelp.co.uk/construction-costing-boq-error-management-sample-42897

Native Assignment Help. (Native Assignment Help, 2026)

https://www.nativeassignmenthelp.co.uk/construction-costing-boq-error-management-sample-42897

- FreeDownload - 35 TimesUnit 4: Leadership and Management Assignment Sample

Introduction: Leadership and Management Assignment This report discovers the...View or download

- FreeDownload - 40 TimesSimilarities and Differences: Milgram's Obedience Study vs. Burger's Replication Assignment Sample

Introduction: Psychology Experiments on Obedience: Milgram and Burger...View or download

- FreeDownload - 39 TimesSports Direct International: Business Simulation and PESTEL Analysis Assignment Sample

Sports Direct International: Business Simulation and PESTEL Analysis Assignment...View or download

- FreeDownload - 43 TimesLevel 3 in Adult Care Assignment

Level 3 in Adult Care Importance of Health and Well-being 1.1 Relationship...View or download

- FreeDownload - 34 TimesCMA4004 Operation And Resource Management Assignment

CMA4004 Operation And Resource Management Assignment Sample Introduction The...View or download

- FreeDownload - 39 TimesSHN4013 Psychological Perspectives On Health And Wellbeing

Introduction The primary purpose of this portfolio is to review a behaviour...View or download

-

100% Confidential

Your personal details and order information are kept completely private with our strict confidentiality policy.

-

On-Time Delivery

Receive your assignment exactly within the promised deadline—no delays, ever.

-

Native British Writers

Get your work crafted by highly-skilled native UK writers with strong academic expertise.

-

A+ Quality Assignments

We deliver top-notch, well-researched, and perfectly structured assignments to help you secure the highest grades.